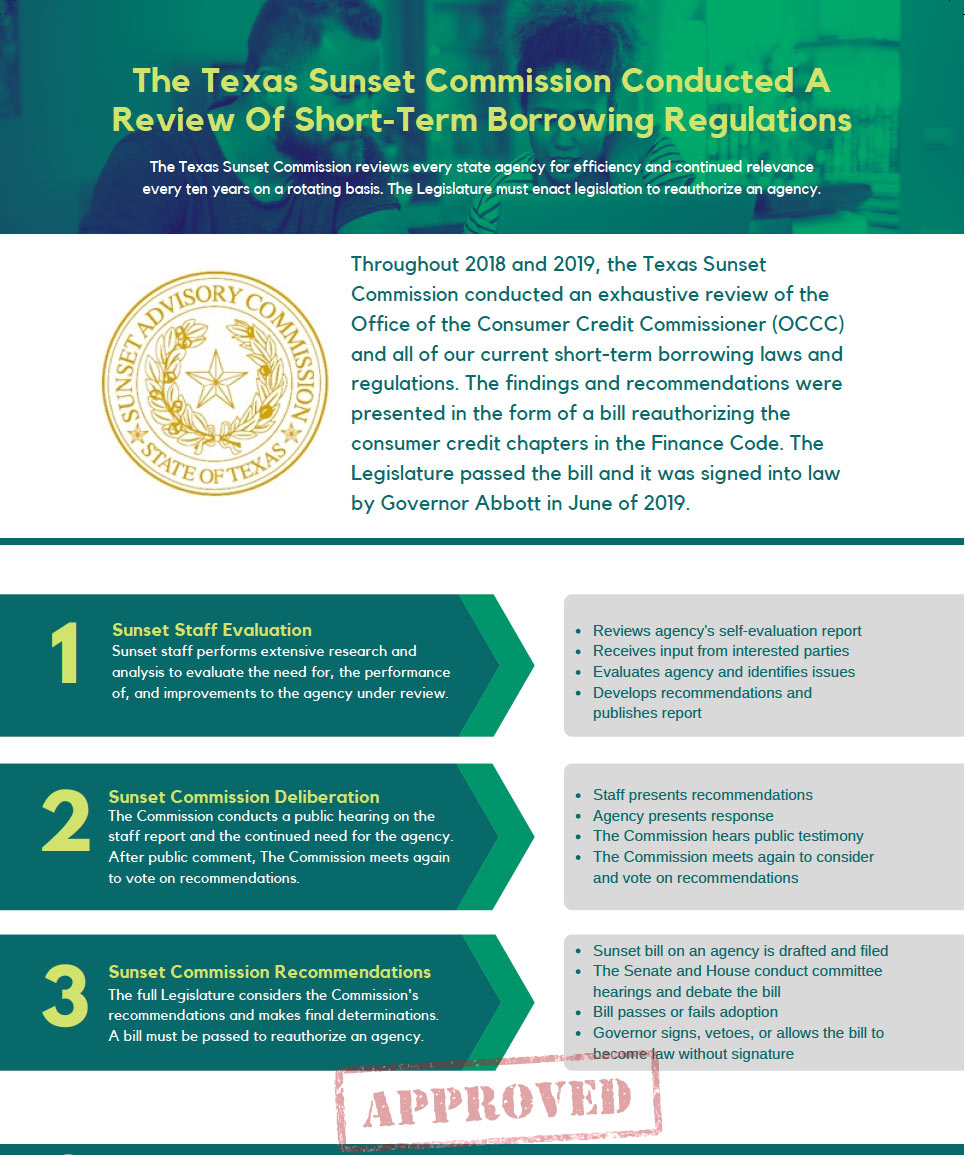

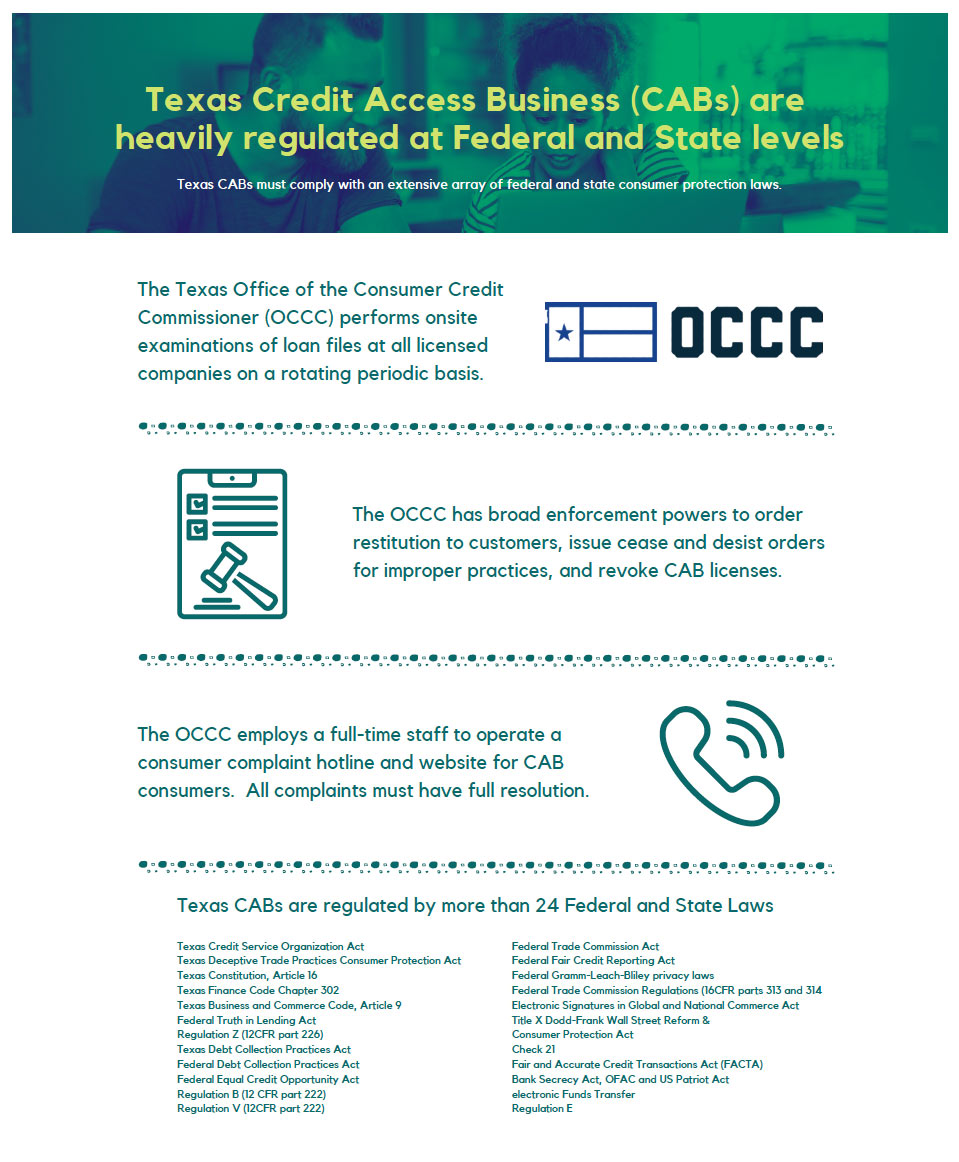

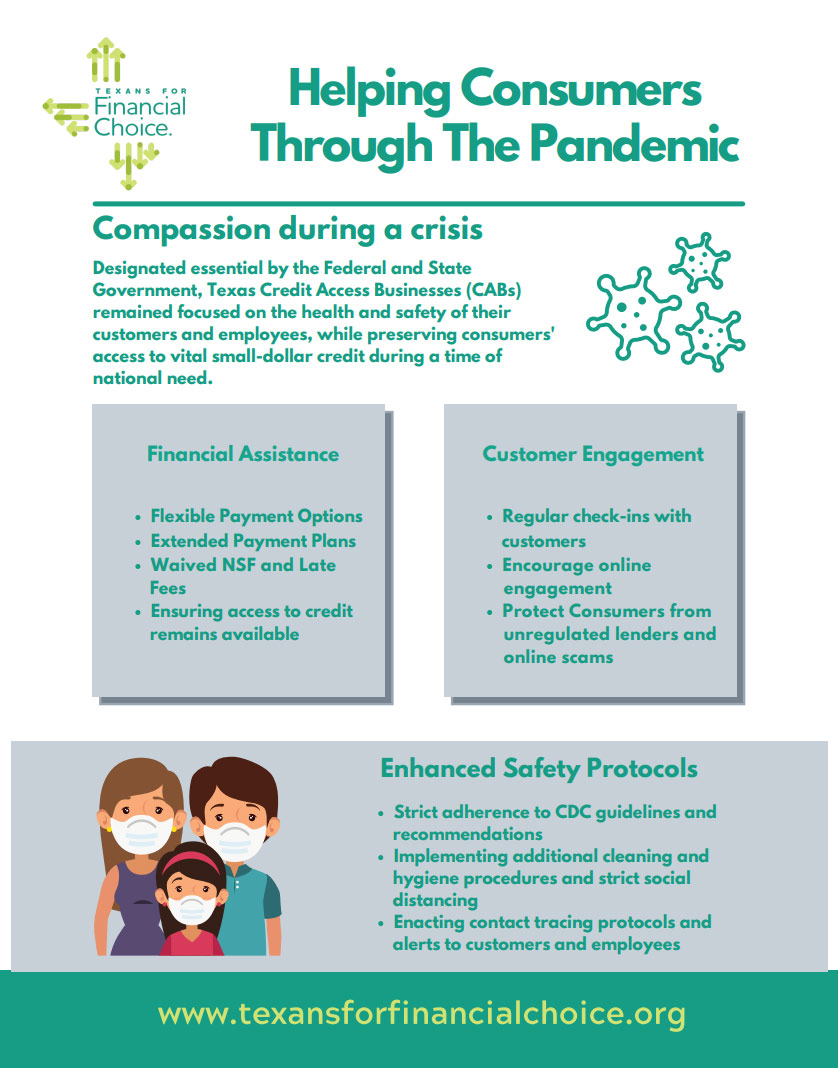

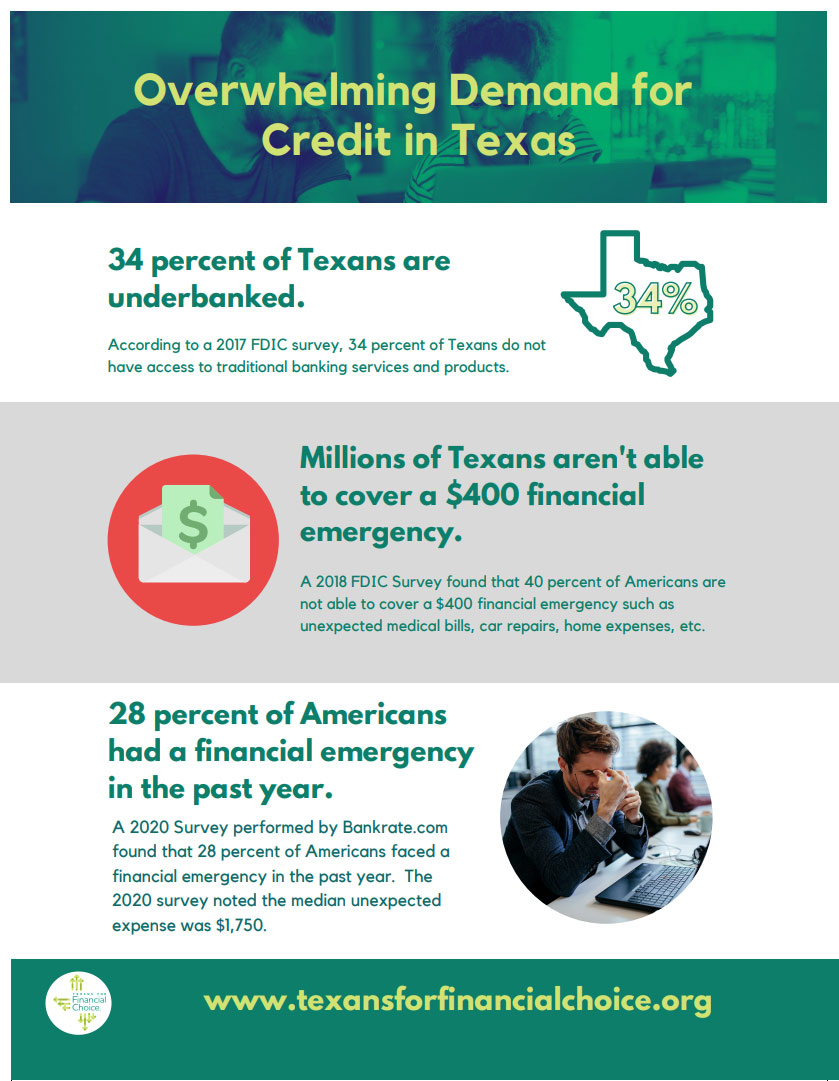

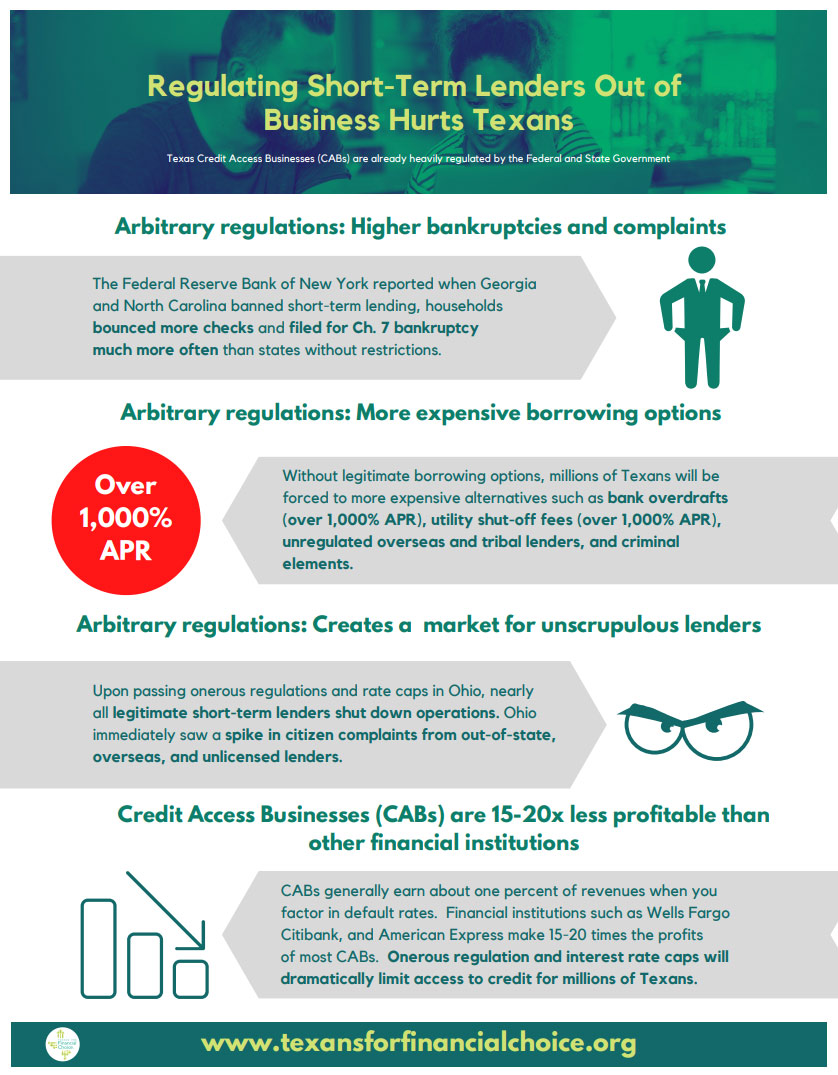

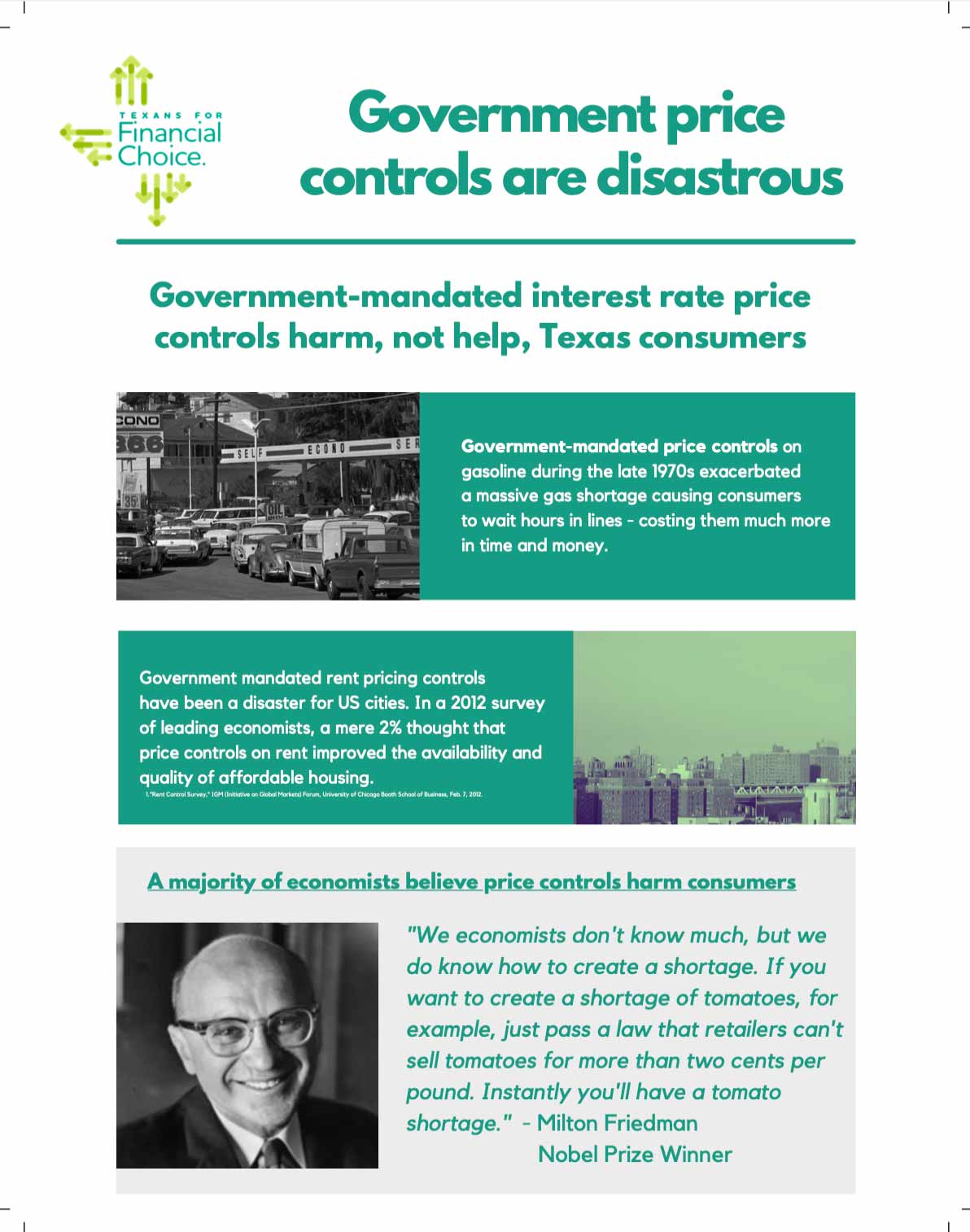

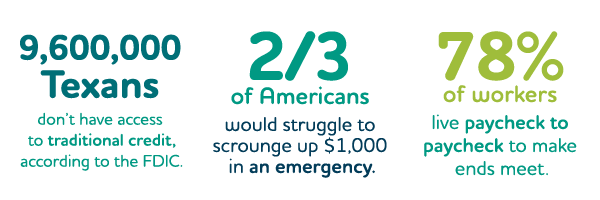

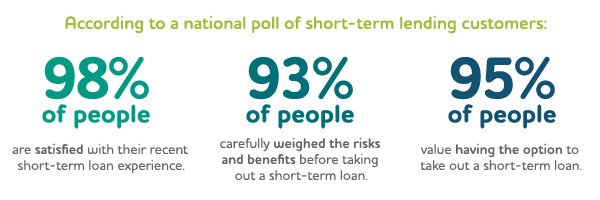

About the Issue TAKE ACTION The Texas Sunset Commission conducted an exhaustive review of short-term borrowing regulations throughout 2018 and 2019 CLICK TO VIEW IN NEW WINDOW Texas short-term borrowing industry is heavily regulated by more than 26 federal and state laws CLICK TO VIEW IN NEW WINDOW The short-term borrowing industry has the lowest complaint rate of all financial services in Texas CLICK TO VIEW IN NEW WINDOW Texas Credit Access Businesses (CABs) helped their borrowers during the Covid-19 Pandemic CLICK HERE TO VIEW IN NEW WINDOW Short-term borrowers carefully weigh the risks, value the products, and are overwhelmingly satisfied with their loan experiences CLICK TO VIEW IN NEW WINDOW Hardworking Texans deserve access to credit in a financial emergency CLICK HERE TO VIEW IN NEW WINDOW Eliminating access to credit hurts, not helps, hardworking Texans CLICK HERE TO VIEW IN NEW WINDOW Opposition to the short-term borrowing industry offer no realistic private-sector credit alternatives other than taxpayer subsidized loans CLICK HERE TO VIEW IN NEW WINDOW There are unintended consequences of government-mandated interest rate caps that hurt Texans. CLICK HERE TO VIEW IN NEW WINDOW Government price controls are disastrous for Texas CLICK HERE TO VIEW IN NEW WINDOW Key Stats